Disclosure: I have been holding shares in CDR since Q4 of 2015.

Today’s post is going to be a bouquet of different topics, revolving around a look back on my encounter with and impressions of the eponymous CD Projekt SA. If you tend to favor a more qualitative approach and prefer growth companies to deep value situations (cigar butts never quite lost that connotation of cancer for me personally) or simply want some insight into the video game industry then this might well be the post for you. But enough idle ink, let us start at the beginning and introduce the company.

The Organizational Structure:

CDR is a Polish holding company founded in 1994 whose two main subsidiaries are engaged in video game development and distribution with a primary but no longer exclusive focus on PC.

The first of these two segments is their development studio, CD PROJEKT RED, which is known for the Witcher games – a trilogy of action-rpgs based on the popular high fantasy book series by author Andrzej Sapkowski. Usually when consumers talk about CDR, they are referring to this segment.

The second and less widely known segment of CDR are GOG Ltd. and GOG Poland Sp. z. o. o. (the latter is the portion of GOG operations focused on domestic distribution whilst GOG Ltd. is its global, and frankly more significant, counterpart) which are concerned with the purely digital distribution of games via the GOG.com domain. Think Steam, but smaller and better curated.

It is not worth worrying too much about the separation of the two GOGs as the company recently adopted a resolution to merge them.

The Backstory:

CDR’s early days and that of its founders, Marcin Iwiński and Michał Kiciński, was fraught and filled with uncertainty. With Soviet influence no longer a major factor in its political and economic policies, Poland had begun to westernize rapidly (if you ignored the politics and the occasional Stalinist relic, you would nowadays be hard-pressed to tell the difference between urban Poland and any other first world economy by the by) and to import new consumer goods such as video games in the process. In this environment, Iwiński and Kiciński founded CDR on a shoestring budget, initially doing localization and distribution work for foreign publishers.

These activities eventually led them to make their own attempt at video game development, a fateful decision which resulted in the release of the first Witcher game in 2007. The game was flawed yet still managed to be a moderately successful release due to the Wiedźmin brand and its mature and gritty take on the fantasy-rpg combination – somewhat of an unclaimed niche in the market as AAA-titles shied away from such risqué themes (and do so to this day), afraid of alienating mass-audiences. It would not be much of an overstatement to say that contemporary publishers thought about projects in two categories only: games that were Call of Duty and games that were not, the latter being untenable investments. Had this not been the case, I doubt CDR would have been able to succeed.

CD Projekt barely survived as it was after White Wolf, a vain effort to bring the Witcher game to console which battered the company financially in 2009. As devastating as the misstep turned out to be, it also proved an important learning experience not to outsource development work. Nevertheless CDR – against all odds – managed both to remain independent and to produce the second Witcher game, Assassins of Kings, which improved very significantly on its predecessor’s gameplay, introduced the franchise to a larger audience and was commercially successful to the point where it enabled CDR to essentially self-publish the third and last installment of the Witcher series in 2015.

Since then, CDR has continued to expand in virtually every metric at an astonishing pace, all the while garnering exceptionally positive reviews, building a large and loyal fan-base and developing several major titles such as GWENT (an online card collecting game based on the Witcher universe not entirely dissimilar to Hearthstone) which is now in closed beta, Cyberpunk 2077 and another as of yet unnamed project.

If you would like to read in more detail about CD Projekt’s past, I highly recommend this article.

The Price:

Seeing as my purchase dates back to the end of 2015 it makes sense to primarily work with the information available then to illustrate my process. A subsequent look at more recent figures will then serve as commentary on my initial analysis (yes, yes, hello hindsight & confirmation bias; assume that I just randomly picked a Polish holding company if that makes you feel like you are standing on more empirically solid ground).

I first bought on November 19th 2015 at a price of 23.93 PLN a share. In the prior months of the year, the price had moved from a low around 17ish to over 27 but gave back some of that appreciation, returning to its lower twenties. This movement turned out to be more or less negligible as you would have been happy to have bought CDR at even a significant premium seeing as the stock closed at 65.60 yesterday. Based on the half-year figures 2015 a price of 23.93 PLN at per share diluted profit of 2.49 PLN implied a P/E of about 9.61. A week before my purchase however, Q3 results were published and the P/E ratio adjusted to the new figures actually decreased to a mind-numbing 8.22 with a per-share profit of 2.91 PLN despite the clear trajectory of growth that was obvious to anyone in the industry (or so I thought, the analysts’ dogs must have been very busy munching on the proverbial homework the day CDR came up).

With The Witcher 3: Wild Hunt having already been released to an enthusiastic crowd (props to the marketing department at CDR) in May, investors on a schedule similar to mine had a whooping 6 months time to form an impression. Not that forming said impression would have required much effort. There was no question that The Witcher 3 was a quantum leap forward in every respect compared to its already well-crafted predecessor. The scope, the level of polish – pun not intended – and technical optimization, the quality and sheer amount of voice-work in multiple languages, the excellent writing, the gameplay… – there was not a single aspect of the product that did not set new standards for the genre (in a competitive industry inhabited by such giants as Activision Blizzard, Microsoft, Square Enix and Sony – just think about that for a minute!). It was so brutally obvious that any conscientious investor in the industry practicing Lynch-style product-sniffing should have been tempted to give CDR a look and if it were only to see how much of its bottom-line would be affected by this one game (spoiler alert: the vast majority of it, GOG still quietly chugging along in the background). Nevertheless, the opportunity persisted.

The Business:

The company as such had several other characteristics of interest besides its modest price and a net profit margin in the forties (you heard me). First, CDR’s balance sheet had been strengthened significantly in light of its precarious past and debt as a whole had been reduced to the point of insignificance (one of the key conditions I set for my investments). And second, GOG, though still very light in its impact on the financials, was and still is attractive as a long-term growing operation per se for several reasons I will quickly summarize below:

- Biggest competitor to Steam, benefits from every controversy Steam stumbles into as it is the most convenient and comprehensive alternative

- Low additional capital requirements for expansion as customer service and site maintenance, the primary cost factors, grow only slowly from baseline with additional sales volume

- Digital sales only means very low distribution costs, very long sale cycles and stable margins

- Synergy with CD PROJEKT RED releases, duh

- Established niche with good old games (hence GOG); reduces need for making unfavorable deals with new AAA-releases to maintain customer base of platform

- DRM-free (!) in a world with idiotic anti-piracy systems that do not work and punish legitimate consumers

- Good reputation and excellent marketing (cooperation with relevant creators on platforms such as Twitch and Youtube is great reach at low cost)

- Both platforms (Steam client and GOG Galaxy) can coexist reasonably well

I am, as I was then, of the conviction that the GOG segment is going to add significant value especially as the development side of things reaches a scale where management will have to expand considerably. Fortunately that stage lies plenty of miles down the road still. Until then the distribution of its in-house titles (and possibly engines) was, is and likely will remain CDR’s most important endeavor. Let us therefore look at the development side of things next.

Though there exists the perception of gaming as childish and trivial, AAA-level game development is anything but as it requires the coordination of vast groups of people (hundreds to thousands of individuals) with highly specialized skill sets in both the fine arts and high tech. Graphic & animation design, sound design, writing and programming talent have to come together under one creative direction to conceive, test and craft an enjoyable user experience. Games are not interactive films and there are no lucky coincidences or improvisation in their development. Every single part of a game has to be made by someone either directly or via a system that models the instance in question. Oversights or mistakes result in bugs, some of them potentially making the game unplayable. Good game development is really, really difficult. With that and the quality of the Witcher trilogy in mind it was readily apparent that there was some serious brainpower employed at CDR. This in turn meant that current projects were likely of similar quality and even more importantly that the firm was both attractive to experienced workers in the industry and made good hiring decisions – crucial factors if the management was to execute on its ambitious plans for expansion.

Speaking of ambitious plans, I have to say that I was impressed by both their simplicity and boldness:

CD PROJEKT RED business objectives

To be counted among the world’s top three videogame developers; to ensure a lasting place for our brands in the global popular culture.

As I briefly touched upon already, the upper echelons of the video game industry are not known to be pushovers. For a relatively small company in Poland that only a year or two ago stared into the abyss to come out, point at the likes of Ubisoft and Activision Blizzard and announce that they were going to be a serious competitor was not something that I had seen before. If it had been some random tech company I would have ignored such talk as hot air from a CEO trying a bit too hard to pull off the black turtle-neck… yet the reality presented itself very differently indeed. Seeing Kiciński, Iwiński, Nielubowicz and Badowski (joint CEO, “, CFO, studio head) present interim results made it clear that they were perfectly capable not just as individuals but that they shared a common goal with unusual focus. They had gone through the difficult years of the company and survived which showed to me that they had the character of true founders. People like this are the kind of management I envision when thinking about ideal leadership: A singular vision of the company’s future inextricably linked to their ego and perception of self-worth. People like that never prioritize the short over the long-term because they are not constantly eyeing for a profitable exit or personal enrichment at the cost of the enterprise which is so en vogue in tech (cough cough, Evan Spiegel). This type of management also tends to be realistic and measured in their public communications as bragging is a short-term oriented behavior and does not benefit them in the long haul. Another benefit of management that functions as a team is that even in the event of illness or similar misfortune the company does not have to slow down whereas in Job-esque situations things tend to get messy more quickly than you would anticipate even when you are a behemoth like Apple. Some problems simply cannot be solved or sped-up by throwing money at them which I feel is all too easily forgotten by those who sit on heaps of cash. As Wernher von Braun would have put it: Crash programs fail because they are based on the theory that, with nine women pregnant, you can get a baby a month.

There are plenty more things to be mentioned in favor of CDR’s management (such as their reluctance to simply pay out dividends while in their growth stage) but the single most important attribute that management behavior can display is a deep understanding of what they are doing. It may sound simple-minded to you but when it comes to all kinds of IPOs in tech or lifestyle-brands the one question that I would want to see the CEO answer is: what does the company do? If for even a split-second their eyes betray the slightest hint of panic or confusion, their smile cracks or their voice trembles – forget it. Not that I look at IPOs in the first place but my point stands. No-one who does a good job has any trouble explaining to you what it is they do. If they truly love their work it is quite the opposite and they will rant about the most minute details for as long as you let them. It is really really difficult to fake expertise for more than five minutes of conversation. Body-language, a glint in the eye, getting ahead of themselves because they forget that not everyone else has the intimate familiarity with the subject matter they do – there are subtle but unmistakable tells individuals deeply immersed in an area give off. And even beyond that, long-term return on equity trends can serve as strong signals as to the efficacy of administration. Unsurprisingly CDR’s management passes with flying colors as their insistence on long, multi-year development cycles, excellently timed and targeted marketing and consumer-friendliness (again, no DRM) demonstrates that they are not just good leaders but have been molded in their priorities by the dynamics of the industry they are in.

The Industry:

In my view there are two inalienable characteristics to the games industry that will trip up outsiders: One, game development is cyclical on a scale of years moreso than months and two, companies in the space follow rules that make them behave a lot like service companies as opposed to secondary industry (especially when their products have online components like multiplayer features or stores). As a result the most important driver of costs is wages (dependent partially on local cost of living) and there are long dry stretches where sales numbers peter out until they spike massively on the release of a new anticipated title – if the marketing was properly executed.

Another variable which may mitigate or enhance these dynamics is scale. A titan like Ubisoft can stagger releases which smooths out sales because they have several projects under development at all times while a small independent publisher (or indie) has very little ability to do so as they do not have the capacity for multiple releases. AAA-releases nevertheless tend to cluster around two or three busy seasons, the biggest being Christmas for obvious reasons and savvy indies sometimes schedule around that. The clustering of releases can have significant drawbacks as they may end up cannibalizing each other’s audiences which harms sales (sometimes permanently). Larger scale often also means that a publisher has to prioritize marketing for flagship titles at the expense of others and that they can absorb the occasional botched release (which they end up doing surprisingly often). Paradoxically this does not mean that large developers take on more risks and innovate more but au contraire that they ‘play it safe’ by establishing core IPs with mainstream appeal which receive annual or biannual releases that rarely go far beyond moderate iteration or improvement above predecessors. Budgets for these games and their marketing typically extends from dozens to hundreds of millions of USD and they require the sale of millions of copies in order to be profitable (think Hollywood blockbuster). Usually they reach those numbers and are fairly lucrative but sometimes they fail spectacularly.

As every release represents at least a year’s worth of labor and marketing they present the opportunity for both roaring success or abysmal failure. Indies which rarely have the resources for such extravagant spending employ far fewer individuals and develop on lean budgets with grass-root and highly targeted marketing (social media, YouTube etc.) which lets them subsist and even thrive on far lower sales numbers as long as their games are good and priced accordingly (half the amount of a premium title or less). They are however only one or two failures away from being bankrupted at any given time unless they manage to make use of crowdfunding platforms (think Kickstarter) which can be extremely valuable as they present a cheap source of up-front capital, a signal as to the demand for the specific product and a marketing tool all in one. With the bar for success markedly lowered, many indies choose to serve niche audiences with less polished but innovative and unusual interactive experiences. It is not all roses and rainbows though as many such attempts end prematurely with either a flawed product or none at all. Here too budgeting and timing are crucial. With this in mind you will understand that having your headquarters situated in San Francisco or Seattle as opposed to Warsaw or Krakow is a sign of poor judgement indeed as location adds no value to digitally distributed goods but inflates cost of labor and rent. You can probably guess which of these places are home to CDR.

Speaking of which, let us do a quick rundown on where CDR is to be placed in the spectrum of the industry that I have outlined thus far. CDR is:

- Medium-sized in terms of market-cap but employs only hundreds vs the many thousands characteristic of larger publishers

- Located in Poland

- Flush with cash and has no meaningful debt or consumer financing operations

In other words, CDR is sitting right in the sweet spot between starving indie and stumbling giant. That alone is valuable as it offers the company room for action. But freedom of action and competent leadership is only a good thing if the guiding philosophy is sound. And if CDR’s history of decision-making is anything to go by it is.

Competitive Advantages:

CDR has an exceptional understanding of its target audience and what they expect and wish for as evidenced by its ability to grow and capitalize on a reputation for consumer-facing practices (great DLC at fair prices, no DRM, representative marketing) and delivering exceptional value (100+ hours of high-end interactive entertainment for 50 bucks; try to kill 100 hours with films at that price point – you cannot do it). Their games have consistently been praised by critics and gamers alike (a line which is very blurred as CDR understand very well) because of a thoughtful and engaging portrayal of meaningful choice, sexuality and violence (HBO’s handle on these themes looks utterly clumsy and immature in comparison) in fleshed-out worlds that are populated by layered and interesting characters. Because CD Projekt fully comprehends the power of word of mouth and targeted marketing in the era of social media (where every customer can potentially become an unpaid brand-advocate) it should not come as a surprise to learn that they managed to grow from catering purely to a niche audience to becoming a brand with mass-appeal not in spite but because of their refusal to compromise the vision of their products. Turns out that not insulting your customers’ intelligence is not such a bad idea after all when your business model heavily relies on user satisfaction and repeat patronage, color me shocked.

I could go on about the many excellent choices CDR have made but I think we might be approaching the point of diminishing returns. Just a last one for the road: Not rushing development. So many AAA-titles are pushed out the door too early because of unrealistic scheduling. Here is the thing about rushing games though: It is like pushing chicks from the nest before they figure out how to take flight – it is wasteful and a mess where no one benefits as the bulk of expenses has already been incurred and a much better pay-off often is only a few months away. Making a great game takes years and CDR have been known to afford their projects as much time as they need and no less. Believe it or not but paying customers remember which companies consistently release unpolished buggy messes that crash every half hour and which ones do the opposite even when the problems are patched away over time. You only get one first impression. People get tired of bad releases and develop considerable loyalty to brands that deliver. After all, which cordwainer would you opt for, the one who sells boots with holes in them but promises to fix them down the line or the one selling proper ones in the first place? It really is not rocket science but major publishers sure make it look like it.

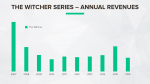

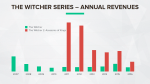

Now, maybe you are not convinced by my portrayal of the story. Perhaps you would prefer to see some evidence for how good CDR’s track record has been. Fair enough. Here are a set of graphs clarifying the growth in sales with each release of the trilogy.

The complete presentation with actual numbers can be viewed here: fy-2016-financial-results-presentation-2.

Let me remind you that even the first release was quite satisfactory in its own right. Overall the Witcher games have sold more than 25 million copies. Remember the trajectory of growth that I was going on about earlier? Well this is it, it does not get any clearer than these colored bars.

How can it be that an upstart like CDR experiences such commercial success? Well, if you have read my post about what makes a good business then you will recognize the two pillars: Management & staff and structural nature of the industry. I have already addressed the former but only hinted at the latter. So let us talk a little bit about why people play games in the first place or put slightly differently, where video games add value to consumers’ lives.

What you often hear said about gaming is that it is at best a waste of time and at worst a dangerous addiction. Especially mentally confined individuals will even tell you that games cause violence and are to blame for school shootings (I do not have much to say about these claims except that reality and data simply do not support them whatsoever). Ultimately games are nothing more or less than another medium for content comparable to film and books. What value derive people from movies and books? It varies from person to person and instance to instance but primarily media serve to inform or misinform, educate and entertain. In our case the focus lies decidedly on entertainment. Games are an excellent tool of storytelling and escapism because their interactive nature immerses and requires the continuous participation of the player in ways that films and books cannot. Therefore the underlying question is not what value is added by games as such but by entertainment in general.

Questions such as this one of course are difficult to answer in some sense because they start tugging at the fabrics of our ideology and cultural perceptions. What is clear however, is that entertainment has to be adding some form of economic value somewhere because if it were not so humanity would not have evolved so uniformly to develop such rich and varied frameworks for its creation and consumption. There is not a single civilization that does not have its own ways of temporarily escaping reality through storytelling which indicates that it must have profound utility in the framework of natural selection beyond merely being enjoyable. Ultimately life is harsh and I suspect that the telling of stories not only helps with the creation and maintenance of community (which is clearly advantageous) but that in some sense it is what keeps us going. Distraction from suffering, a sense of progress and achievement and space for self-expression – this is what gaming provides to hundreds of millions. If that is not worth the occasional 60 bucks then I do not know what is.

Because of this utility in staving off existential dread the video game industry differs from the consumer goods tag it is routinely labeled with when it comes to the demand behavior of its customers. It is very difficult to satiate demand for good games because it rises in line with marketing and strong products. Think about it: Has there ever been an oversupply of great films? Of course not! Cult cinema or great writing can attract vast audiences in times of abundance and in times of dearth. Truly exceptional works that concern the human condition are timeless. Excellent games too have the potential for very long shelf-lives, especially when their distribution and storage is digital and thus very cheap. When keeping a particular title on sale costs you very little and your costs per unit are virtually nothing even relatively low sales numbers add up over the years. That is why digital distribution à la GOG and good quality control in game development are the way to go.

At this point let me summarize the competitive advantages of CDR for the people who like things to be spelled out for them. They are:

- Excellent management

- Well funded, can self-finance from operations

- Attractive industry

- Attractive location

- Room and ambition for sustainable growth

- Strong brand & marketing

- Very capable staff with deep expertise

If you have read this far you now have glimpsed how important intangible qualities are in this industry and why CDR was such an unusual opportunity. Situations like this can never be fully understood with balance sheets and income statements alone but need to be properly contextualized. The old-school deep value investors could never have profited from this type of scenario because book value simply does not capture the actual worth of service companies. This is what buying a great company at a fair price looks like to me.

Closing Words:

This investment will long stay in my memory as an example of just how far accountant’s disease and superficial bias can separate value and price even in a bull market. I can only speculate as to what reasoning led potential investors to sneer at this opportunity. Some may have thought Poland third-world. Others perhaps did not want to associate themselves with something they considered to be as childish as gaming. Possibly there simply is not that large of an overlap of investors and gamers who would have had the ability to judge marketing and products. Ultimately it does not matter and I am glad to have been in the right place at the right time.

I hope this has been of interest to you.

Tom

Ps: You know a game developer means business when they start lobbying the government.