Everything anyone consumes has to be made by someone. Every good, every service; cornflakes, iPhones, math lessons, homes, condoms, physiotherapy sessions, belts, hats, cheese sandwiches – even 3B pencils. Every. Single. Thing.

It may be that you think of this as not a particularly profound observation. ‘Well, obviously!’ – you mutter to yourself.

Judging by collective human behavior, it does not seem to be quite so obvious. Take any boom and bust cycle. The expansionary part of such a cycle is intuitive. There is stuff. There are humans. Humans want the stuff. They take the stuff. Simple.

Of course, it does not quite end there. After a while, the stuff starts running out. Humans still want the stuff. Uh-oh. So what do they do? The first response is rationing. Restricting consumption of stuff works in the sense that on paper, consuming less stuff makes the stuff run out less quickly. Naturally it does not solve the problem that humans still want the stuff. In fact, some perverse dynamics may lead humans to covet the stuff even more, now that it is hard to get. They start tampering with the rules. Some humans end up getting a lot of the stuff – more than they need even – and others less. In other words, a social hierarchy emerges around the distribution of stuff.

Hierarchy, however, creates incentive for conflict. After all, why should that guy (let us call him Larry) get so much stuff if I, Livius, do not get enough stuff to sate my own desires? Maybe if I demonstrate that I deserve the stuff more than Larry, I can just… take more of the stuff. There are several ways that this can play out.

Postponement

Livius: “Larry, I have meditated deeply on this matter and I think I deserve more of the stuff. You have stuff. Give me your – I mean, my – stuff.”

Larry: “No.”

Livius: “Hm, o.k.”

Livius and Larry ignore the conversation ever happened and try to go their separate ways in the future. They may quarrel again later – perhaps with entirely different parties.

Violence

Livius: “Larry, I have meditated deeply on this matter and I think I deserve more of the stuff. You have stuff. Give me your – I mean, my – stuff.”

Larry: “No.”

Livius: “Hm, o.k.”

*Livius whacks Larry over the head with a pointy rock and takes the stuff anyway*

Actually, rock-mediated conflict resolution has very much gone out of fashion with the emergence of complicated and deep hierarchies that have evolved ‘sophisticated’ organs and structures to reduce friction costs from conflict. While the idea of violence may conjure up images of youths in partner look carrying projectile accelerators, the vast majority of conflict in society is settled through non-physical and indirect (and in aggregate cheaper forms of) violence: politics, laws, prison systems, social norms, intimidation and so forth.

Alignment

Livius: “Larry, I have meditated deeply on this matter and I think I deserve more of the stuff. You have stuff. Give me your – I mean, my – stuff.”

Larry: “No.”

Livius: “Hm, o.k.”

Larry: “How about we team up instead and take the stuff from someone else and then divide it amongst ourselves?”

Livius: “Eh, sounds good to me.”

Livius and Larry begin co-operating and pooling resources, potentially making them more competitive and improving their access to stuff.

No matter which scenario(s) plays out, these are the basic options available to humans when it comes to the distribution of resou- I mean, stuff. All agent interaction in one way or another follows one or a combination of these dynamics.

But what about the supply side? So far, we have been laboring under the assumption that the number of units of stuff available for consumption is fixed. That is not quite right. So back to the drawing board.

There is stuff. Humans take the stuff. The stuff runs out. Humans make more stuff. And they lived happily ever after.

The crux is the mis-match between the rate at which humans generate stuff and the rate at which humans would like to consume it. Though theoretically human capacity for the production of goods and services in absolute terms trends toward infinity, over any finite period of time, the amount of stuff produced remains finite itself. A variable yet constrained supply of stuff and the ability of humans to generate it in limited quantities over time (yet always desiring higher present consumption than present production), however, allows for the emergence of something very interesting indeed: credit.

Credit allows for the expedition of consumption (i.e. bringing it forward into an earlier period) relative to what would otherwise be possible under the constraint of having to provide equivalent productive output in exchange at the moment of acquisition of a good or service. In other words: Magic!

In an idealized world where future output of individuals is known, credit/lending would be an essentially risk-free affair that would not command significant fees. In reality however, credit is of course risky because future repayment is not assured and therefore lending demands compensation. But that is not the only difference that arises from uncertainty about future production. Inflation, of course, is a significant concern – as is financial repression. Yet these are ultimately manifestations of a different underlying problem. Because lending always involves a creditor and a debtor, both of whom have opposed interests in a narrow sense (if they truly had completely opposite goals, lending would not occur at all which would be disastrous for mankind), unproductive loans (that is to say the additional productive output generated as a result of the spending enabled by the loan is less than the principal plus interest charged) represent a miscalculation – a shortfall – in coordinating present consumption with future production which has to be covered out of the pocket of either one or both the parties involved.

This fact – that borrowing may not always be paid for completely out of the borrower’s pocket – leads to (unproductive) credit becoming a tool for wealth redistribution. But not just to the detriment of future humans to the benefit of present humans, even across socioeconomic and geopolitical divides. Credit is an extremely potent instrument that can – in the (right? wrong?) hands – reshuffle social hierarchy or maintain an existing order. Furthermore, credit is inherently non-democratic and intellectually opaque even to the so-called experts. At least when a nuclear warhead hits a city, most people can establish who executed the sequence of actions that has led to the destruction (and most of them also intuitively grasp the cost of having leveled a city and killed large numbers of productive civilians). Not necessarily so with the redistribution of wealth resulting from the use of credit.

Just picture our previous exchange between Livius and Larry in an environment where credit is an established social institution.

Livius: “Larry, I have meditated deeply on this matter and I think I deserve more of the stuff. You have stuff. Give me your – I mean, my – stuff.”

Larry: “Certainly. Please just sign here, here and here. Interest payable semi-annually.”

Livius: “Hm, o.k.”

Now, dear reader, tell me: Who is the winner in this situation? Is it Livius, because he received purchasing power he did not have before this exchange? Is it Larry, because he will in the end receive satisfactory return on his principal? Is it both, because the loan is invested productively and leads to a sustainable increase in output attributable to Livius who uses some of it to cover the debt? Is it neither, because the purchasing power is spent unproductively and Larry is not compensated?

Go on.

.

..

…

Don’t look at me – I have no clue either.

The true nature of the transaction depends entirely on its terms and ultimate repayment. But without fully knowing – or understanding – the terms, much less knowing the future, we cannot know how or in what direction wealth was redistributed. Nevertheless, redistribution has been and is occurring. At scale.

Indeed, even if credit were not such an enormous system spanning all of human civilization and you only had a small amount of lending going on, the dynamics of causality (investors affectionately call this compounding) must transform the course of history completely, given time. If there is the possibility of capital accumulation and there are flows of credit, even if every agent begins with exactly the same amount of capital, uncertainty and randomness will make some of them wealthy and powerful and some of them poor and weak. This issue is exacerbated by the fact that wealthy individuals have easier and cheaper access to credit and may indeed end up being (the) creditors themselves.

This is the beauty of humanity: Be confronted with a harsh physical reality dictated by the universe, create a sophisticated buzzing perpetuum mobile of social organs that allow prolonged ignoring of reality to the point of complete delusion about fundamental physical truth, have the miracle-machine break down eventually and be thrown into despair, all the while crying out: “Woe is us, how could anyone have seen it coming that one cannot in aggregate consume more than one produces for a prolonged period of time?”. Who needs children in order to witness true surprise and wonder at a new discovery when we have the financial industry and credit cycles?

At this point we could get into government intervention into lending, central banks or the looming contraction of global credit but each is a world unto its own of such magnitude that I shall address them in a separate piece.

This is a topic I have wanted to write about for a while yet never quite found the right moment for. Then, cryptocurrency entered mainstream ‘awareness’ and I started thinking about how one would price non-productive, cash-less assets if someone put a gun to your head and did not accept the rough (but probably fairly close to the truth) estimate of zero. It quickly became apparent, that extending the value framework to cash-flow-free assets required thinking about the very core of value and why/how it works. That is what this very compact post is about. Though I am likely to revisit this topic in more detail in the future, I hope that his snippet will prove worth the read nonetheless.

In value investing, intrinsic price (often called value) of an asset (or a collection thereof, e.g. a firm) is determined by discounting the sum of all future generated cash flows. The cash flow part is fairly self-explanatory but tricky in a couple of ways, such as cash flows being unequally distributed over time (‘lumpy’), inflation, the fundamental uncertainty of their occurrence and magnitude in the first place and so on. The process of discounting is supposed to account for these hurdles in pricing the nominal cash flows but is affected also by the current ‘risk-free rate of return’ which is strongly determined (and proxied) by interest rates (via treasury bills and the like).

I personally have a few problems with the notions of risk and return that prevail in finance today but the underlying concept of ‘cheaper’ returns (in other words, greater risk-adjusted returns) in a competitive market warranting, ceteris paribus, less nominal discounting (up until it is priced in line with its alternatives after adjustment for risk and asset characteristic preferences) is, of course, sound [basically, people want to maximize their risk-adjusted, preference-weighted returns and compare the choices available to them and because they compete, better deals tend to get arbitraged away].

What is crucial to understand is that value investing is, ultimately, a pricing framework. Of course it also values assets but it does so in order to ultimately help price them! It appears to me very dangerous to forget the purpose of the value philosophy and succumb to moralistic notions of value being the superior metric of measurement just because the investor happens to believe so or has been told so by a supposed authority. An investor who hopes to properly serve his function as a capital delegator (others might prefer the term capital allocator which I think is taking too much credit in the grand scheme) ought to think like a craftsman with his models of pricing and capital as tools and raw material, respectively. If the hammer does not effectively accomplish the task at hand then considerations should be made both as to whether there is need for a different tool and as to whether the endeavor is worthwhile as such.

Now, of course, thought should also be given to the reason why a certain tool is particularly well- or ill-suited for this task (say, of pricing). How come a fundamental/value approach is an excellent tool-set for the long-term pricing of cash-flow producing assets? In this case, it is because the value philosophy better recognizes the most important causal factor driving price trends in the long-term: the asset’s capacity to generate profit (which of course comes from cash flow).

But what is profit? Long-term sustainableProfit is the result of cost-efficient monetization of the creation of utility for customers!

With this in mind, it should become clear why profits drive long-term prices (but I will elaborate nonetheless because I enjoy reading my own opinion back and nodding in agreement).

The key to seeing the fundamental implications of a utility-based view of profit lies in understanding utility and why humans (and organisms in general) pursue it over time. Quite simply, it is because of natural selection! Organisms that do not pursue behavior that seeks to maximize utility tend to go extinct and/or do not reproduce very much. Behavior that maximizes utility is behavior that tends to maximize reproductive fitness and vice-versa. So over time, the number of agents that are utility-maximizing as a fraction of all agents asymptotically approaches 1 (i.e. they dominate).

Put yet another way, the sustainability (i.e. the characteristic of something to stick around and propagate over time) of a behavior is intimately linked to the sustainability of the agent that executes the behavior. For a behavior to be long-term, it needs to stick around (be sustainable).

So, what do all agents that influence prices over time have in common (because they have to in order to be able to affect prices)? They are able to buy or sell. To be able to buy and/or sell, an agent needs to be active (that is be alive/functional – which of course implies having been born/existing). They also need to be able to effect such a transaction – they need assets that are accepted in exchange (currency, equity, etc.; in our current system, anything that is monetizable).

And that is why natural selection matters in markets just as it does nearly everywhere else: Markets and transactions can only ever be dominated in the long-term by agents that are executing behavior that is seeking to maximize reproductive fitness (otherwise they would not be around/a significant factor). Since this behavior correlates with the pursuit of utility, customers who purchase goods and services tend to buy in ways that tend to maximize utility. This means that firms need to maximize cost-efficient creation of utility for customers in order to sustainably maximize long-term positive cash flows (profits!). Furthermore, it is these cash flows that fuel wages of workers and profits of owners. The money, in other words, which allows market participants to buy and sell! Therefore markets (including stock markets) are dominated, over time, by people seeking to maximize positive long-term cash-flow as they have both greater numbers and greater financial means to do so in the long-term. This applies to stock markets as well and hence to the price-trends of securities. Consequently, pricing frameworks that focus on the security-underlying firm’s long-term profitability prospects (such as value/fundamental investing) outperform frameworks that do not. This overall dynamic is also the reason why functioning capitalist systems inevitably are wealth- and utility creators.

I hope you found this bit of foundational theory intriguing

Disclosure: I have been holding shares in CDR since Q4 of 2015.

Today’s post is going to be a bouquet of different topics, revolving around a look back on my encounter with and impressions of the eponymous CD Projekt SA. If you tend to favor a more qualitative approach and prefer growth companies to deep value situations (cigar butts never quite lost that connotation of cancer for me personally) or simply want some insight into the video game industry then this might well be the post for you. But enough idle ink, let us start at the beginning and introduce the company.

The Organizational Structure:

CDR is a Polish holding company founded in 1994 whose two main subsidiaries are engaged in video game development and distribution with a primary but no longer exclusive focus on PC.

The first of these two segments is their development studio, CD PROJEKT RED, which is known for the Witcher games – a trilogy of action-rpgs based on the popular high fantasy book series by author Andrzej Sapkowski. Usually when consumers talk about CDR, they are referring to this segment.

The second and less widely known segment of CDR are GOG Ltd. and GOG Poland Sp. z. o. o. (the latter is the portion of GOG operations focused on domestic distribution whilst GOG Ltd. is its global, and frankly more significant, counterpart) which are concerned with the purely digital distribution of games via the GOG.com domain. Think Steam, but smaller and better curated.

It is not worth worrying too much about the separation of the two GOGs as the company recently adopted a resolution to merge them.

Source: cdprojekt.com/en/capital-group

The Backstory:

CDR’s early days and that of its founders, Marcin Iwiński and Michał Kiciński, was fraught and filled with uncertainty. With Soviet influence no longer a major factor in its political and economic policies, Poland had begun to westernize rapidly (if you ignored the politics and the occasional Stalinist relic, you would nowadays be hard-pressed to tell the difference between urban Poland and any other first world economy by the by) and to import new consumer goods such as video games in the process. In this environment, Iwiński and Kiciński founded CDR on a shoestring budget, initially doing localization and distribution work for foreign publishers.

These activities eventually led them to make their own attempt at video game development, a fateful decision which resulted in the release of the first Witcher game in 2007. The game was flawed yet still managed to be a moderately successful release due to the Wiedźmin brand and its mature and gritty take on the fantasy-rpg combination – somewhat of an unclaimed niche in the market as AAA-titles shied away from such risqué themes (and do so to this day), afraid of alienating mass-audiences. It would not be much of an overstatement to say that contemporary publishers thought about projects in two categories only: games that were Call of Duty and games that were not, the latter being untenable investments. Had this not been the case, I doubt CDR would have been able to succeed.

CD Projekt barely survived as it was after White Wolf, a vain effort to bring the Witcher game to console which battered the company financially in 2009. As devastating as the misstep turned out to be, it also proved an important learning experience not to outsource development work. Nevertheless CDR – against all odds – managed both to remain independent and to produce the second Witcher game, Assassins of Kings, which improved very significantly on its predecessor’s gameplay, introduced the franchise to a larger audience and was commercially successful to the point where it enabled CDR to essentially self-publish the third and last installment of the Witcher series in 2015.

Since then, CDR has continued to expand in virtually every metric at an astonishing pace, all the while garnering exceptionally positive reviews, building a large and loyal fan-base and developing several major titles such as GWENT (an online card collecting game based on the Witcher universe not entirely dissimilar to Hearthstone) which is now in closed beta, Cyberpunk 2077 and another as of yet unnamed project.

If you would like to read in more detail about CD Projekt’s past, I highly recommend this article.

The Price:

Seeing as my purchase dates back to the end of 2015 it makes sense to primarily work with the information available then to illustrate my process. A subsequent look at more recent figures will then serve as commentary on my initial analysis (yes, yes, hello hindsight & confirmation bias; assume that I just randomly picked a Polish holding company if that makes you feel like you are standing on more empirically solid ground).

I first bought on November 19th 2015 at a price of 23.93 PLN a share. In the prior months of the year, the price had moved from a low around 17ish to over 27 but gave back some of that appreciation, returning to its lower twenties. This movement turned out to be more or less negligible as you would have been happy to have bought CDR at even a significant premium seeing as the stock closed at 65.60 yesterday. Based on the half-year figures 2015 a price of 23.93 PLN at per share diluted profit of 2.49 PLN implied a P/E of about 9.61. A week before my purchase however, Q3 results were published and the P/E ratio adjusted to the new figures actually decreased to a mind-numbing 8.22 with a per-share profit of 2.91 PLN despite the clear trajectory of growth that was obvious to anyone in the industry (or so I thought, the analysts’ dogs must have been very busy munching on the proverbial homework the day CDR came up).

With The Witcher 3: Wild Hunt having already been released to an enthusiastic crowd (props to the marketing department at CDR) in May, investors on a schedule similar to mine had a whooping 6 months time to form an impression. Not that forming said impression would have required much effort. There was no question that The Witcher 3 was a quantum leap forward in every respect compared to its already well-crafted predecessor. The scope, the level of polish – pun not intended – and technical optimization, the quality and sheer amount of voice-work in multiple languages, the excellent writing, the gameplay… – there was not a single aspect of the product that did not set new standards for the genre (in a competitive industry inhabited by such giants as Activision Blizzard, Microsoft, Square Enix and Sony – just think about that for a minute!). It was so brutally obvious that any conscientious investor in the industry practicing Lynch-style product-sniffing should have been tempted to give CDR a look and if it were only to see how much of its bottom-line would be affected by this one game (spoiler alert: the vast majority of it, GOG still quietly chugging along in the background). Nevertheless, the opportunity persisted.

The Business:

The company as such had several other characteristics of interest besides its modest price and a net profit margin in the forties (you heard me). First, CDR’s balance sheet had been strengthened significantly in light of its precarious past and debt as a whole had been reduced to the point of insignificance (one of the key conditions I set for my investments). And second, GOG, though still very light in its impact on the financials, was and still is attractive as a long-term growing operation per se for several reasons I will quickly summarize below:

Biggest competitor to Steam, benefits from every controversy Steam stumbles into as it is the most convenient and comprehensive alternative

Low additional capital requirements for expansion as customer service and site maintenance, the primary cost factors, grow only slowly from baseline with additional sales volume

Digital sales only means very low distribution costs, very long sale cycles and stable margins

Synergy with CD PROJEKT RED releases, duh

Established niche with good old games (hence GOG); reduces need for making unfavorable deals with new AAA-releases to maintain customer base of platform

DRM-free (!) in a world with idiotic anti-piracy systems that do not work and punish legitimate consumers

Good reputation and excellent marketing (cooperation with relevant creators on platforms such as Twitch and Youtube is great reach at low cost)

Both platforms (Steam client and GOG Galaxy) can coexist reasonably well

I am, as I was then, of the conviction that the GOG segment is going to add significant value especially as the development side of things reaches a scale where management will have to expand considerably. Fortunately that stage lies plenty of miles down the road still. Until then the distribution of its in-house titles (and possibly engines) was, is and likely will remain CDR’s most important endeavor. Let us therefore look at the development side of things next.

Though there exists the perception of gaming as childish and trivial, AAA-level game development is anything but as it requires the coordination of vast groups of people (hundreds to thousands of individuals) with highly specialized skill sets in both the fine arts and high tech. Graphic & animation design, sound design, writing and programming talent have to come together under one creative direction to conceive, test and craft an enjoyable user experience. Games are not interactive films and there are no lucky coincidences or improvisation in their development. Every single part of a game has to be made by someone either directly or via a system that models the instance in question. Oversights or mistakes result in bugs, some of them potentially making the game unplayable. Good game development is really, really difficult. With that and the quality of the Witcher trilogy in mind it was readily apparent that there was some serious brainpower employed at CDR. This in turn meant that current projects were likely of similar quality and even more importantly that the firm was both attractive to experienced workers in the industry and made good hiring decisions – crucial factors if the management was to execute on its ambitious plans for expansion.

Speaking of ambitious plans, I have to say that I was impressed by both their simplicity and boldness:

CD PROJEKT RED business objectives

To be counted among the world’s top three videogame developers; to ensure a lasting place for our brands in the global popular culture.

As I briefly touched upon already, the upper echelons of the video game industry are not known to be pushovers. For a relatively small company in Poland that only a year or two ago stared into the abyss to come out, point at the likes of Ubisoft and Activision Blizzard and announce that they were going to be a serious competitor was not something that I had seen before. If it had been some random tech company I would have ignored such talk as hot air from a CEO trying a bit too hard to pull off the black turtle-neck… yet the reality presented itself very differently indeed. Seeing Kiciński, Iwiński, Nielubowicz and Badowski (joint CEO, “, CFO, studio head) present interim results made it clear that they were perfectly capable not just as individuals but that they shared a common goal with unusual focus. They had gone through the difficult years of the company and survived which showed to me that they had the character of true founders. People like this are the kind of management I envision when thinking about ideal leadership: A singular vision of the company’s future inextricably linked to their ego and perception of self-worth. People like that never prioritize the short over the long-term because they are not constantly eyeing for a profitable exit or personal enrichment at the cost of the enterprise which is so en vogue in tech (cough cough, Evan Spiegel). This type of management also tends to be realistic and measured in their public communications as bragging is a short-term oriented behavior and does not benefit them in the long haul. Another benefit of management that functions as a team is that even in the event of illness or similar misfortune the company does not have to slow down whereas in Job-esque situations things tend to get messy more quickly than you would anticipate even when you are a behemoth like Apple. Some problems simply cannot be solved or sped-up by throwing money at them which I feel is all too easily forgotten by those who sit on heaps of cash. As Wernher von Braun would have put it: Crash programs fail because they are based on the theory that, with nine women pregnant, you can get a baby a month.

There are plenty more things to be mentioned in favor of CDR’s management (such as their reluctance to simply pay out dividends while in their growth stage) but the single most important attribute that management behavior can display is a deep understanding of what they are doing. It may sound simple-minded to you but when it comes to all kinds of IPOs in tech or lifestyle-brands the one question that I would want to see the CEO answer is: what does the company do? If for even a split-second their eyes betray the slightest hint of panic or confusion, their smile cracks or their voice trembles – forget it. Not that I look at IPOs in the first place but my point stands. No-one who does a good job has any trouble explaining to you what it is they do. If they truly love their work it is quite the opposite and they will rant about the most minute details for as long as you let them. It is really really difficult to fake expertise for more than five minutes of conversation. Body-language, a glint in the eye, getting ahead of themselves because they forget that not everyone else has the intimate familiarity with the subject matter they do – there are subtle but unmistakable tells individuals deeply immersed in an area give off. And even beyond that, long-term return on equity trends can serve as strong signals as to the efficacy of administration. Unsurprisingly CDR’s management passes with flying colors as their insistence on long, multi-year development cycles, excellently timed and targeted marketing and consumer-friendliness (again, no DRM) demonstrates that they are not just good leaders but have been molded in their priorities by the dynamics of the industry they are in.

The Industry:

In my view there are two inalienable characteristics to the games industry that will trip up outsiders: One, game development is cyclical on a scale of years moreso than months and two, companies in the space follow rules that make them behave a lot like service companies as opposed to secondary industry (especially when their products have online components like multiplayer features or stores). As a result the most important driver of costs is wages (dependent partially on local cost of living) and there are long dry stretches where sales numbers peter out until they spike massively on the release of a new anticipated title – if the marketing was properly executed.

Another variable which may mitigate or enhance these dynamics is scale. A titan like Ubisoft can stagger releases which smooths out sales because they have several projects under development at all times while a small independent publisher (or indie) has very little ability to do so as they do not have the capacity for multiple releases. AAA-releases nevertheless tend to cluster around two or three busy seasons, the biggest being Christmas for obvious reasons and savvy indies sometimes schedule around that. The clustering of releases can have significant drawbacks as they may end up cannibalizing each other’s audiences which harms sales (sometimes permanently). Larger scale often also means that a publisher has to prioritize marketing for flagship titles at the expense of others and that they can absorb the occasional botched release (which they end up doing surprisingly often). Paradoxically this does not mean that large developers take on more risks and innovate more but au contraire that they ‘play it safe’ by establishing core IPs with mainstream appeal which receive annual or biannual releases that rarely go far beyond moderate iteration or improvement above predecessors. Budgets for these games and their marketing typically extends from dozens to hundreds of millions of USD and they require the sale of millions of copies in order to be profitable (think Hollywood blockbuster). Usually they reach those numbers and are fairly lucrative but sometimes they fail spectacularly.

As every release represents at least a year’s worth of labor and marketing they present the opportunity for both roaring success or abysmal failure. Indies which rarely have the resources for such extravagant spending employ far fewer individuals and develop on lean budgets with grass-root and highly targeted marketing (social media, YouTube etc.) which lets them subsist and even thrive on far lower sales numbers as long as their games are good and priced accordingly (half the amount of a premium title or less). They are however only one or two failures away from being bankrupted at any given time unless they manage to make use of crowdfunding platforms (think Kickstarter) which can be extremely valuable as they present a cheap source of up-front capital, a signal as to the demand for the specific product and a marketing tool all in one. With the bar for success markedly lowered, many indies choose to serve niche audiences with less polished but innovative and unusual interactive experiences. It is not all roses and rainbows though as many such attempts end prematurely with either a flawed product or none at all. Here too budgeting and timing are crucial. With this in mind you will understand that having your headquarters situated in San Francisco or Seattle as opposed to Warsaw or Krakow is a sign of poor judgement indeed as location adds no value to digitally distributed goods but inflates cost of labor and rent. You can probably guess which of these places are home to CDR.

Speaking of which, let us do a quick rundown on where CDR is to be placed in the spectrum of the industry that I have outlined thus far. CDR is:

Medium-sized in terms of market-cap but employs only hundreds vs the many thousands characteristic of larger publishers

Located in Poland

Flush with cash and has no meaningful debt or consumer financing operations

In other words, CDR is sitting right in the sweet spot between starving indie and stumbling giant. That alone is valuable as it offers the company room for action. But freedom of action and competent leadership is only a good thing if the guiding philosophy is sound. And if CDR’s history of decision-making is anything to go by it is.

Competitive Advantages:

CDR has an exceptional understanding of its target audience and what they expect and wish for as evidenced by its ability to grow and capitalize on a reputation for consumer-facing practices (great DLC at fair prices, no DRM, representative marketing) and delivering exceptional value (100+ hours of high-end interactive entertainment for 50 bucks; try to kill 100 hours with films at that price point – you cannot do it). Their games have consistently been praised by critics and gamers alike (a line which is very blurred as CDR understand very well) because of a thoughtful and engaging portrayal of meaningful choice, sexuality and violence (HBO’s handle on these themes looks utterly clumsy and immature in comparison) in fleshed-out worlds that are populated by layered and interesting characters. Because CD Projekt fully comprehends the power of word of mouth and targeted marketing in the era of social media (where every customer can potentially become an unpaid brand-advocate) it should not come as a surprise to learn that they managed to grow from catering purely to a niche audience to becoming a brand with mass-appeal not in spite but because of their refusal to compromise the vision of their products. Turns out that not insulting your customers’ intelligence is not such a bad idea after all when your business model heavily relies on user satisfaction and repeat patronage, color me shocked.

I could go on about the many excellent choices CDR have made but I think we might be approaching the point of diminishing returns. Just a last one for the road: Not rushing development. So many AAA-titles are pushed out the door too early because of unrealistic scheduling. Here is the thing about rushing games though: It is like pushing chicks from the nest before they figure out how to take flight – it is wasteful and a mess where no one benefits as the bulk of expenses has already been incurred and a much better pay-off often is only a few months away. Making a great game takes years and CDR have been known to afford their projects as much time as they need and no less. Believe it or not but paying customers remember which companies consistently release unpolished buggy messes that crash every half hour and which ones do the opposite even when the problems are patched away over time. You only get one first impression. People get tired of bad releases and develop considerable loyalty to brands that deliver. After all, which cordwainer would you opt for, the one who sells boots with holes in them but promises to fix them down the line or the one selling proper ones in the first place? It really is not rocket science but major publishers sure make it look like it.

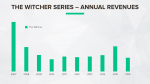

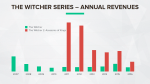

Now, maybe you are not convinced by my portrayal of the story. Perhaps you would prefer to see some evidence for how good CDR’s track record has been. Fair enough. Here are a set of graphs clarifying the growth in sales with each release of the trilogy.

Let me remind you that even the first release was quite satisfactory in its own right. Overall the Witcher games have sold more than 25 million copies. Remember the trajectory of growth that I was going on about earlier? Well this is it, it does not get any clearer than these colored bars.

How can it be that an upstart like CDR experiences such commercial success? Well, if you have read my post about what makes a good business then you will recognize the two pillars: Management & staff and structural nature of the industry. I have already addressed the former but only hinted at the latter. So let us talk a little bit about why people play games in the first place or put slightly differently, where video games add value to consumers’ lives.

What you often hear said about gaming is that it is at best a waste of time and at worst a dangerous addiction. Especially mentally confined individuals will even tell you that games cause violence and are to blame for school shootings (I do not have much to say about these claims except that reality and data simply do not support them whatsoever). Ultimately games are nothing more or less than another medium for content comparable to film and books. What value derive people from movies and books? It varies from person to person and instance to instance but primarily media serve to inform or misinform, educate and entertain. In our case the focus lies decidedly on entertainment. Games are an excellent tool of storytelling and escapism because their interactive nature immerses and requires the continuous participation of the player in ways that films and books cannot. Therefore the underlying question is not what value is added by games as such but by entertainment in general.

Questions such as this one of course are difficult to answer in some sense because they start tugging at the fabrics of our ideology and cultural perceptions. What is clear however, is that entertainment has to be adding some form of economic value somewhere because if it were not so humanity would not have evolved so uniformly to develop such rich and varied frameworks for its creation and consumption. There is not a single civilization that does not have its own ways of temporarily escaping reality through storytelling which indicates that it must have profound utility in the framework of natural selection beyond merely being enjoyable. Ultimately life is harsh and I suspect that the telling of stories not only helps with the creation and maintenance of community (which is clearly advantageous) but that in some sense it is what keeps us going. Distraction from suffering, a sense of progress and achievement and space for self-expression – this is what gaming provides to hundreds of millions. If that is not worth the occasional 60 bucks then I do not know what is.

Because of this utility in staving off existential dread the video game industry differs from the consumer goods tag it is routinely labeled with when it comes to the demand behavior of its customers. It is very difficult to satiate demand for good games because it rises in line with marketing and strong products. Think about it: Has there ever been an oversupply of great films? Of course not! Cult cinema or great writing can attract vast audiences in times of abundance and in times of dearth. Truly exceptional works that concern the human condition are timeless. Excellent games too have the potential for very long shelf-lives, especially when their distribution and storage is digital and thus very cheap. When keeping a particular title on sale costs you very little and your costs per unit are virtually nothing even relatively low sales numbers add up over the years. That is why digital distribution à la GOG and good quality control in game development are the way to go.

At this point let me summarize the competitive advantages of CDR for the people who like things to be spelled out for them. They are:

Excellent management

Well funded, can self-finance from operations

Attractive industry

Attractive location

Room and ambition for sustainable growth

Strong brand & marketing

Very capable staff with deep expertise

If you have read this far you now have glimpsed how important intangible qualities are in this industry and why CDR was such an unusual opportunity. Situations like this can never be fully understood with balance sheets and income statements alone but need to be properly contextualized. The old-school deep value investors could never have profited from this type of scenario because book value simply does not capture the actual worth of service companies. This is what buying a great company at a fair price looks like to me.

Closing Words:

This investment will long stay in my memory as an example of just how far accountant’s disease and superficial bias can separate value and price even in a bull market. I can only speculate as to what reasoning led potential investors to sneer at this opportunity. Some may have thought Poland third-world. Others perhaps did not want to associate themselves with something they considered to be as childish as gaming. Possibly there simply is not that large of an overlap of investors and gamers who would have had the ability to judge marketing and products. Ultimately it does not matter and I am glad to have been in the right place at the right time.

I came across a post titled Pseudo-quants that is in all honesty pretty dumb but gives me an excuse to rant for a bit so I will take it. Please enjoy the fruits of my mild ennui.

The gist of the article (it is quite short so by all means do go ahead and read it if you feel my summation might be unfair) goes roughly like this: A reference to this article by Jason Zweig followed by a jab at Rob Arnott’s funds in particular and factor-investing- and smart-beta-type funds in general, stating that they did not perform like investments by ‘real’ quants which the author goes on to describe as mathematicians who enter the business without a background in finance and who (or so the writer insinuates) consider themselves distinct from more traditional investors. The author then attempts to explain the reasons behind this distinction (finance is not a science, nothing works forever in finance, the scientific method cannot be applied to finance, all evidence indicates that academic finance has failed miserably), denounces the Sveriges Riksbank Prize in Economic Sciences (which in all fairness I do agree is somewhat bad taste) bashes finance some more because of its supposed inability to make predictions and ends (not a moment too soon) by declaring pseudo-scientific funds’ cataclysmic downfall.

Oh my.

Let us begin with the whole ‘pseudo-quant funds are underperforming’ spiel that is rife with bias of the not-so-subtle kind. Comparing the multi-decade outperformance of Renaissance Technologies to five years of a recently struggling all asset fund to imply the objective superiority of quantitative investing is about as meaningful as racing Usain Bolt against a moderately competent scavenger hunt enthusiast… in a marathon. It is all sorts of misrepresentative. Different time periods, underlying assets, goals & benchmarks and stages in their life-cycle (Might the author have intentionally cherry-picked a fund down on its luck instead of a top performer among its kind more analogous to Renaissance Technologies? I certainly think so) – for a post on a site claiming to oppose fraudulent financial advice this looks pretty dodgy. But OK, maybe the person with a background in mathematics (presumably; no indication as to who the author/s might be) is just bad at contextualizing data.

Finance is not a science

Finance is not a science but an art – sayeth our anonymous author. That may be true. Also true however is the fact that many of the tools used in finance are no less rooted in science than say mathematics seeing as that is precisely whence they stem (could not resist). It seems a tad dismissive to discount the merit of an entire (and comparatively young) field employing the scientific method and its tools on the basis that the scale of its subject matter is messier than that of particle physics. Finance, like engineering, may not be a science in the way that geology fits the category but it certainly is not completely random voodoo to the point of uselessness either, far from it. And regarding predictions I would say those of finance do not lag far behind the ones of evolutionary biology. It is functionally impossible to say with specificity how a species might change over the course of millions of years but we nevertheless have a framework of natural selection and are indubitably richer because of it. Prediction need not purely refer to foreseeing specific future events. Describing the dynamics of a system in the abstract in order to better understand the patterns of real life definitely qualifies. Finance is terrible because it is not science is a silly excuse for a logical argument.

Nothing works forever in finance

It is not untrue that markets tend to erode easily quantifiable trends over time due to competing participants. That is the nature of the game. But that applies not just for traditional funds but also (even especially) for quants. This is the opposite of an argument for and I quote:

Clearly, the most successful quant funds do not consider academic finance as part of the quant world. Let us understand why.

The scientific method cannot be applied to finance.

The scientific method can be applied to literally anything. Even finance. That is the point.

All evidence indicates that academic finance has failed miserably

Really? Not most or some evidence? All of it. Huh. The more you know.

Where are the billionaire financial academics? There are no billionaire Nobel Prize winners in Economics. If you could make accurate financial predictions, would you not act on them, if for no other reason to prove a point? No academic financial theory has generated substantial investment returns for their authors.

Academics are precisely that. Their work revolves around research and understanding and not monetary gain (in a perfect world that is). And perhaps there is more to getting rich than just having the know-how. What about access to capital, personal ambition, networking and luck?

Also: economics is not primarily concerned with wealth management but with the functioning of economies. Economics != finance. There are plenty of billionaires with a finance background.

The gullibility crisis

Many investors have been misled to believe that financial products originated in academic finance are scientific. Pension allocators have poured hundreds of billions of dollars in so-called “factor investments” and “smart beta funds”, not because they perform well, but because they have a good academic pedigree.

I do not think that investors have been misled for the most part but rather that they lack financial literacy, restraint and are constrained by structural dynamics that disconnect incentives from long-term performance. If anything it is not people’s trust in science that is exploited but their willingness to obey authority figures. There indeed are bad apples in the world of finance – quants included.

And that’s a key flaw of academic financial models, that they are public: Humans will always find a way to turn a purported financial “law” on its head, and profit from those gullible enough to believe in it.

Right, every single human being has the inclination and resources to exploit market trends… That is why momentum does not exist – no wait. This is not how it works. And since when are finance papers concerned with figuring out how to beat the market? That is the job of active investors. CAPM, EMH & co. are attempts to dissect how and why pricing mechanisms in markets play out the way they do, not recipes to outsmart them.

I could go on about the many flaws and misconceptions of that post but I really do not feel any need to do so. As you can see, even among the people lamenting the taking of false credit there are those brazenly feigning expertise.

The following few paragraphs originally were part of another post still under construction but they hurt its flow and somehow seemed out of place in their self-containedness, so I am putting them here. Hopefully you will find them of interest.

What makes a good Business

An outstanding business rests on a foundation of two equally indispensable pillars. One is the intrinsic nature of its operations, the other is its management and employees. Let me elaborate a little bit on what I mean by that.

The nature or structure of operations fundamentally makes the organization what it is as such. You would not call the postal service a postal service if it primarily sold limbless cold-blooded vertebrates with gills, now would you? At that point you would call it a large-scale distributor of fish and various other goods or perhaps you would refer to it as ‘the sodding reason why my mail reeks of halibut’.

Clearly an organization will take on the characteristics of its underlying operations and behave accordingly. If for a prolonged period of time it does not, then either you have misunderstood its primary activity (maybe the umbrella-retailer whose sales-volume is uncorrelated with the weather is not really selling classic umbrellas but a status-symbol made desirable by ingenious marketing and therefore more suitably categorized as a luxury/lifestyle brand) or there is some fishiness (Herbalife anyone?) going on.

But classification issues aside, any organization is ultimately limited by the characteristics of its operations. If what a business offers is at its core broken, already available in sufficient quantities or unattractive (be it because of inefficient production, it simply not adding value to the customer’s life or a combination thereof) the venture in its entirety will not be a good long-term investment. A pyramid or Ponzi scheme (or simply a terrible business) for instance must collapse eventually, on the very simple basis that its activities do not add net value. Yes, purchasing power shifts from one party to another but the system as a whole is endothermic and needs constant external input to be sustained and be able to grow. A real business’ operations on the other hand behave exothermically, meaning that even without constant outside financing it can sustain and potentially grow itself. An attractive operation is able to sustainably fuel itself from internal cash-flows. Zero exceptions. This is one of the pillars.

The other supporting element is of course people (how anthropocentric) – that is management & employees. They are who is responsible for the optimization of the metrics of underlying operations (no matter if their characteristics are awful, great or somewhere in-between). The management itself cannot change the natural dynamics of a business or industry beyond pushing the enterprise to be as efficient as possible. Good management can however recognize if an operation is attractive in the long-term and adapt depending on the verdict by expanding in terms of scale, commencing a different type of operation entirely, terminating an unattractive operation or enacting an appropriate mix of these measures. Warren Buffett’s acquisition and subsequent transformation away from textiles of Berkshire Hathaway is an example of excellent management and its limits. Even the leadership at Berkshire could not mitigate the problems of the coeval textile industry (reliant on continuous heavy investment, very volatile demand, requiring trained labor in fluctuating numbers) to a sufficient degree and so the only correct choice was to attempt an ordered retreat to greener pastures such as insurance – which obviously succeeded spectacularly. Still, even Warren Buffett could not avoid terminating unattractive operations in the long-term. Management results are totally dependent on operations. Thus a company’s unsatisfactory performance in the short-term does not necessarily indicate bad management or staff but bad long-term results decidedly do. This is the other hallmark of an excellent business: Good management over time reduces unattractive operations of a business and increases attractive ones.

Next time you are struggling to decide if a company is a great enterprise, look at the two pillars. If either one is missing you have your answer.

Plenty of people and institutions fail as investors – there is no two ways about it. There is however an abundance of reasons why they do so (as it turns out Investing is pretty hard, who knew?) and many of them are actually quite interesting to think about, especially when they start involving questions about the nature of the market itself. After all, who does not love a good rant about EMH, active vs. passive or good old animal spirits?

In this post I am not going to talk about any of them.

Instead I want to address the far more mundane but crucial role of proper financial planning in investing. Yes, that is right, I am fun at parties.

What is financial planning? Bluntly put it is the taking of adequate measures (e.g. saving) to ensure that at no point one’s financial obligations (i.e. expenditures & debt) exceed one’s ability to satisfy them (via income & assets). Successful financial planning balances one’s limited resources with as many of one’s personal goals and desires as possible without ever jeopardizing the fulfillment of all needs. Ultimately this enables the individual to lead a lifestyle that is both fulfilling & provides a high quality of life (relative to their means) and is sustainable in the long-term.

To understand what sustainability in the long-term has to do with volatility related risks, we need to look at the rationale behind investing in the first place. A rational agent chooses to invest because they expect their investments to return on resources employed (principal, time, effort) at a rate that is satisfactory compared with all other available alternatives over the chosen time period. There is only one scenario wherein an investor like this can be negatively affected by the volatility of their investments unrelated to their underlying performance: They choose to sell at an inopportune time (that is to say they abandon a position at a level of valuation which prices it below its reasonably expected value based on fundamentals). Note that this does not necessarily mean a net loss in absolute terms but rather underperformance compared to simply maintaining the position. Why would a rational agent that is aware of the true value of their position ever choose to sell at a sub-optimal price? Well, they would not… Unless they were forced to.

How might an investor be forced to prematurely liquidate their holdings? The answer is simple: they need money to cover their obligations. It does not matter why they need the money, if it is because of life-saving heart surgery, insufficient collateral for positions on margin or needing to pay rent, the outcome is the same: underperformance compared to the potential returns of the investment. This is especially damaging from the fundamental investor’s point of view because they are entering positions that are (ideally of course) under-priced and that tend to appreciate nonlinearly over time (as they are better understood or more correctly valued for other reasons) rather than linearly (an investment growing and performing in line with expectations/valuation). In other words, investments are by necessity volatile and if you have to leave the ship at the wrong time, you will get wet, even if it does end up reaching the harbor.

My point is that akin to real life, under good or mediocre conditions you are the biggest threat to your own well-being even if you are perfectly rational (which you are not, cue the ghost of Leonard Nemoy glaring disapprovingly). By taking a conservative approach and investing only what you can afford to lose without having to reduce your standard of living, volatility on its own will never impact your decision making as an investor. Doing so will not automatically cause your investments to be a success but letting volatility affect your decisions is a sure-fire way to snatch defeat even from the jaws of victory.